En raison d'une grève chez bpost, des retards de livraison peuvent survenir. Besoin de quelque chose en urgence ? Optez pour un retrait en magasin ou rendez-vous dans une Librairie Club à proximité.

- Retrait en 2 heures

- Assortiment impressionnant

- Paiement sécurisé

- Toujours un magasin près de chez vous

En raison d'une grève chez bpost, des retards de livraison peuvent survenir. Besoin de quelque chose en urgence ? Optez pour un retrait en magasin ou rendez-vous dans une Librairie Club à proximité.

- Retrait en 2 heures

- Assortiment impressionnant

- Paiement sécurisé

- Toujours un magasin près de chez vous

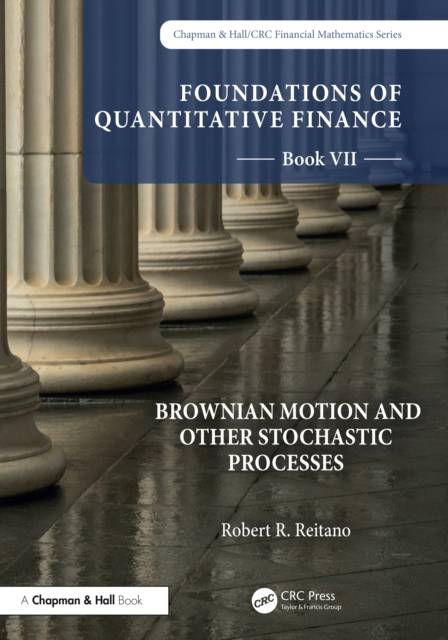

Foundations of Quantitative Finance, Book VII

Brownian Motion and Other Stochastic Processes

Robert R Reitano

160,45 €

+ 320 points

Format

Description

This is the seventh book in a set of ten published under the collective title of Foundations of Quantitative Finance. It introduces and develops properties of Brownian motion as well as two other classes of stochastic processes: Markov processes and martingales. It is for researchers and practitioners of quantitative finance.

Spécifications

Parties prenantes

- Auteur(s) :

- Editeur:

Contenu

- Nombre de pages :

- 363

- Langue:

- Anglais

- Collection :

Caractéristiques

- EAN:

- 9781032229591

- Date de parution :

- 28-04-26

- Format:

- Livre broché

- Format numérique:

- Trade paperback (VS)

- Dimensions :

- 178 mm x 254 mm

- Poids :

- 662 g

Seulement chez Librairie Club

+ 320 points sur votre carte client de Librairie Club

Cadeau

Les avis

Nous publions uniquement les avis qui respectent les conditions requises. Consultez nos conditions pour les avis.